Stock-Based Compensation: How to Use the Backsolve Method Under ASC 718

If you audit or manage a startup company or other privately held business, don’t overlook the treatment of stock-based compensation. If you do, the financials might not stand up to an audit, which could compromise the company’s capital-raising efforts going forward.

As many of you know, startup companies have many cash-intensive challenges such as creating a product, hiring talent and establishing a brand to name a few. Since these activities don’t currently produce cash startups are in a constant battle between raising capital and reigning in cash expenses. Equity compensation is a useful way to conserve precious cash while directly aligning employee goals with company goals and investor goals. Equity compensation usually takes the form of additional equity class(es) in what is already a complex equity structure.

Despite its many benefits, however, equity compensation creates compliance burdens. When auditors evaluate a company’s expenses and liabilities, they need a fair value to assign to those issued equity units. While a time-strapped CFO might have some an idea about what the company is worth, that is not sufficient documentation to withstand audit or regulatory scrutiny. Also, it does not address the specific value of the equity units involved. Risking a qualified opinion is not a good option for any company, let alone one trying to raise capital.

So, what to do?

As I’ve discussed before, the contingent claims analysis (the “CCA”) provides a reliable means for allocating the fair value of equity across the various classes of units. However, the CCA only provides a pathway from total equity value to a per-unit value. As a precursor, we still need to establish equity value, most likely through the discounted cash flow (“DCF”) method. The strength of the DCF method is also its weakness. By incorporating every conceivable variable in a company’s financial outlook, DCF provides a strong basis for fair value.

The DCF process is difficult given the number of variables that it incorporates. DCF is even more complicated for startup companies that don’t have historic results as a guide for potential future performance. Additionally, a startup’s tax outlook can be complicated by a series of net operating losses, amortized research expenditures, and various credits. These factors create many highly variable assumptions that can have a material impact on the company’s fair value.

Fortunately, there is another option that can more easily produce reliable results. It’s called the Backsolve Method which is based on the theory underpinning the CCA. When you think about how the CCA works, you might wonder why we even use the CCA instead of considering a waterfall as of the valuation date?

For example, let’s say preferred equity is 25% of a company’ s outstanding equity and the remainder is common. While it may be practical to talk about the equity structure, the differences in distribution rights are key to understanding the value. Thus, we need to understand the value for each dollar of distribution in which earlier dollars are worth more than later dollars. That’s because earlier dollars require a lower exit threshold. Additionally, the thresholds between distributions to different equity classes affect downside risk and upside potential. This requires a nuanced analysis to describe.

Real world example

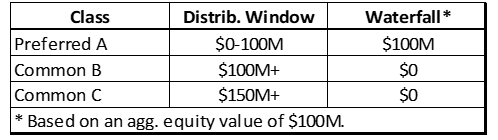

ABC Co. is a startup company whose mission is to use artificial intelligence for early detection of cancer. The company’s CFO reliably pegged ABC Co.’s equity value at $100 million. The company is pre-revenue and likely not looking at a sale, an IPO, or other type of liquidity event for at least five years. Further, the company’s equity structure consists of Series A preferred units with a liquidation preference of $100 million, as well as Series B common units, and Series C common units (only entitled to distributions in a liquidity event in excess of $150 million). If we consider a waterfall, then all of the common units are worth nothing. However, if the company successfully exits five years later at $500 million, then the common units would be entitled to a significant distribution. We do know that A + B + C = E, however we cannot establish the specific value of A, B, or C in our existing framework.

Source: DeJoy & Co. 2024

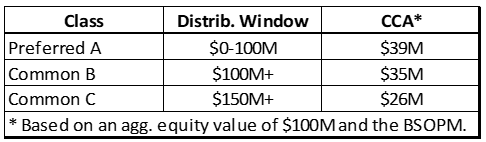

Enter the CCA, which implores us to view each equity class as a call option on equity above a certain distribution threshold.

Through a series of option models, we can distribute the equity value across the preferred and common units. As an input to those option models, we are required to establish a few variables. Some of those variables are objective and others are subjective but based on comparable data. Conducting such an exercise for ABC Co. may yield results like these below:

Source: DeJoy & Co. 2024

These results make more sense than the waterfall method given our understanding of valuation.

Additionally, once we have locked in the variables in our option pricing models (OPMs), the CCA creates a specific relationship between equity value and each equity class, or E ↔ A, E ↔ B, and E ↔ C. The CCA is a great tool to use in this situation where we have a reliable equity value, but it’s useless when we don’t.

The Backsolve Method is a variant of the guideline transaction method. As a primer, the guideline transaction method looks at a transaction in a similar company, which allows us to impute a value for our subject interest. This method is not often used because it can be difficult to find transactions in comparable companies along with the translation over to our subject company. However, if we found a comparable transaction that included all the details in a company that was identical to our subject company, it would be a great start.

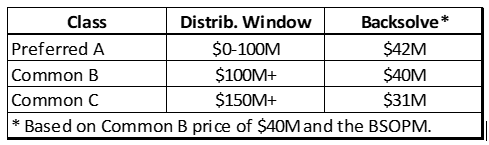

Let’s go back to our example of ABC Co. If the Series B common units recently sold in an arm’s length transaction for $40M, then what is the fair value of the Series C common units? Well, we have a great guideline transaction for starters. Using the CCA we know that B ↔ E ↔ C, or more simply stated, B ↔ C using the transitive property. Using the Backsolve Method, let’s see what the fair value of the Series C common units is:

We can imply a value of $31M for the Series C common units and an aggregate equity value of $113M. Notably, I’ve accomplished this without the cumbersome DCF method.

For startups with recent capital raises, the Backsolve Method can help determine the fair value of equity compensation in congruence with ASC 718. While this can simplify the process, there are still complexities and pitfalls associated with a complex equity structure. Hiring a qualified appraiser who is experienced in valuing equity interests in similar scenarios can be helpful for documenting the analysis properly and for effectively communicating the conclusion to the auditors and other stakeholders.

To summarize, the Backsolve Method helps establish a value for equity compensation based on the latest round of financing or transaction support. The main advantage of using this method is to derive the value of an entity that is based on the previous transaction or financing round and it helps ascertain a value for the equity compensation. This is the main factor that differentiates the Backsolve Method from other methods.

Conclusion

The Backsolve Method is particularly well suited for companies with multiple classes of equity ownership, since these organizations tend to have complex capital structures. Backsolve takes this into consideration while calculating the total equity. This approach makes the value to be as accurate as possible. The option-based equation was created for the OPM Backsolve Method. This equation can also be used to determine the value of equity compensation while using other methods to determine the total equity value.

If you or someone close to you has concerns about stock based compensation, Contact me any time to discuss.

Anthony Venette, CPA/ABV is a Senior Manager, Business Valuation & Advisory, DeJoy & Co., CPAs & Advisors in Rochester, New York. He provides business valuation and advisory services to corporate and individual clients of DeJoy.