We May Never See a Better Environment for Transferring Wealth… Here’s Why

It may seem that there will always be time to address estate planning. However, a unique opportunity to maximize the amount of wealth that can be tax-efficiently passed to heirs will expire at the end of 2025. Furthermore, legislation could curb lifetime exemption limits even sooner. The opportunity is even more pressing because the current market downturn represents an especially advantageous time to optimize your taxable estate before markets eventually recover.

In this article, we explain why 2023 is an ideal year to prioritize your wealth transfer plans.

Current Tax Laws Double Lifetime Giving Exemption

For affluent individuals and their families, estate taxes can represent one of their largest tax liabilities. IRS rules allow certain amounts of an estate to be transferred free of taxes to family and friends, on an annual basis (the limit is $17,000 per person in 2023) and also grant each taxpayer a lifetime giving exemption. Beginning in 2010, that lifetime exemption was $5 million per person indexed for inflation. The Tax Cuts and Jobs Act (TCJA) roughly doubled the giving limit, raising the lifetime exemption in 2023 to $12.92 million for individuals and $25.84 million for married couples.[1]

The caveat—and it’s a big one—is that those expanded exclusion amounts expire at the end of 2025, with lifetime exemption totals reverting back to an estimated $6.40 million per person.[2] Individuals and families seeking to lower their taxable estate may not see such a generous opportunity from the government again, so it’s critical to develop giving plans and put them into motion before it’s too late.

Gifting in a Bear Market Is Like Buying Low

Recent stock and bond market selloffs may make you think that now is a risky time to consider giving away a large portion of your estate. But for those in a position to take full advantage of the lifetime exemption, doing nothing could result in burning up much more in potential tax savings than any recent market losses.

In fact, initiating a giving program during a bear market has the possibility to increase the value of your gifts to future generations. When transferring common stock, for example, you can gift more shares when values are down, potentially providing a larger base of appreciation for the recipient. And, as the donor, a downturn means you could be able to transfer a greater portion of your wealth out of your estate.

Transferring the maximum amount allowed on your terms and timetable not only removes those assets and their potential appreciation from your estate, but it can also add meaning to the gifts by allowing you to see your children and grandchildren enjoy those assets during your lifetime.

A Note of Caution

The generation skipping transfer (GST) tax exemption may also come into play if gifts are given to grandchildren. Gifts to grandchildren and subsequent generations have GST tax considerations. The gift tax exemption and the GST tax exemption start off the same (at $12.92M per individual) but can, and often, get used at different rates. If you have never used your gift tax exemption or GST tax exemption, you should be fine. However, you must be careful as a gift can result in both gift tax and GST tax being imposed on that gift.

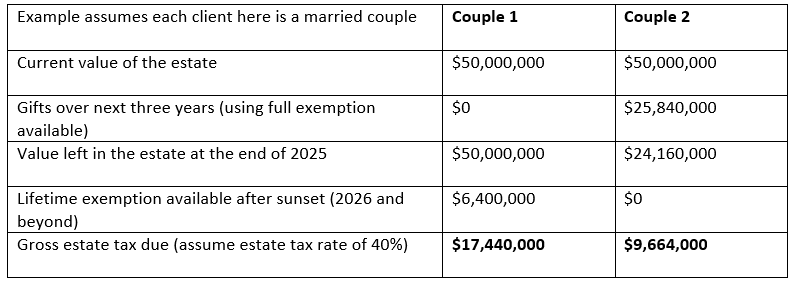

Value of Gifting Today vs. Gifting in the Future

Failure to utilize the full expanded exclusion amount of $12.92 million per individual prior to its lapse at the end of 2025 may result in the unused amount being subject to estate or gift tax.

Key takeaway: An additional $7.78 million is paid in estate taxes by the couple who failed to utilize the expanded exclusion amount before it expires in 2025.

Customize Your Wealth Transfer Strategies

Effective wealth transfer can be accomplished in a number of ways and should be customized to your personal circumstances. Your tax advisor can explain the pros and cons of various gifting options to ensure you receive the full estate tax benefits while retaining a measure of flexibility and access to certain assets if needed. A professional tax advisor can help you prioritize the types of assets to be gifted, such as cash, investments, or business interests.

Various techniques, including using irrevocable trusts and grantor retained annuity trusts (GRATs), can be employed to limit estate taxes when the wealth owner dies. Such trusts are established as a method of transferring wealth out of the owner’s estate for the benefit of family members (e.g., children, grandchildren, etc.). It is important to note that trusts have specific risks and challenges that must be understood before executing transfers of significant wealth. Qualified estate planning advisors also can help identify alternative gifting options, such as promissory notes and intrafamily loans, that may avoid some of the pitfalls of trusts.

When considering how much wealth should be transferred for the benefit of your heirs, thoughtful consideration should be given to how much wealth you should retain in your estate to maintain your lifestyle. Difficult decisions must be made during the estate planning process that weigh current cash flow needs with estate tax savings and preservation of family legacy. A qualified estate planning professional can . model various scenarios to help you determine the amount of gifting that is right for you.

The Clock Is Ticking … Begin the Discussion Now

The window on making the most of the expanded lifetime exemption and shielding a significant portion of your estate from Uncle Sam will close at the end of 2025. We are available to answer many of your questions and help formulate a customized plan that allows you to not just gift your wealth, but gift it with a purpose.

[1] IRS, “IRS provides tax inflation adjustments for tax year 2023,” October 18, 2022

[2] Figure based on estimate of $5 million exemption in 2010 indexed for inflation through 2025

© BDO ALLIANCE 2023 For more information contact Anthony Venette, CPA/ABV.

Anthony Venette, CPA/ABV is a Senior Manager, Business Valuation & Advisory, DeJoy & Co., CPAs & Advisors in Rochester, New York. He provides business valuation and advisory services to corporate and individual clients of DeJoy.